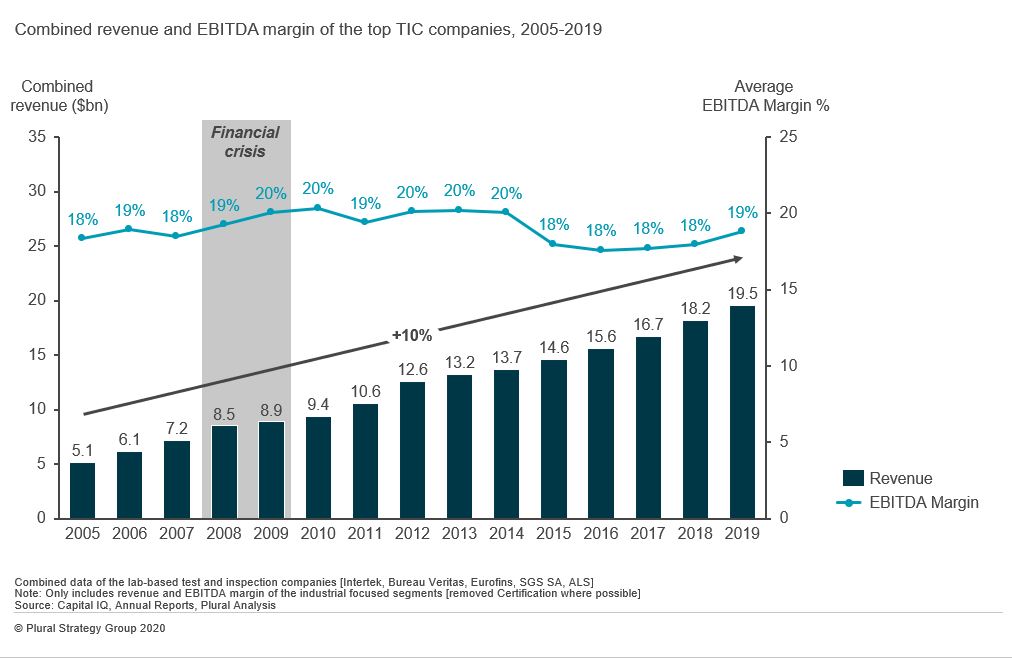

Providers of industrial test and inspection services have impressively resilient business models and have sustained strong margins through market cycles.

Although in-line technology threatens to disrupt the status quo, the traditional lab-based service providers are well entrenched and continue to hold the advantage, partly through access to vast datasets which allows them to produce highly accurate analytics. The rich data is tough to replicate, creating high barriers to entry and placing these firms in poll position to further develop the value proposition to become technology-driven, faster and predictive.

Lab-based test and inspection services are extremely resilient business models due to strong fundamental drivers and high barriers to entry

The test and inspection market is driven by growing globalized demand for regulation of materials/products, the increasing need for guaranteed equipment uptime and increasing corporate outsourcing of testing activities and quality assurance. The industrial-focused test and inspection market is resilient to market downturns as industrial operators are required to test all their machinery for predictive maintenance purposes despite overall declines in production volumes.

Lab-based service providers have the advantage in the industrial test and inspection market as they have the ability to access customer intelligence machine-by-machine and site-by-site from anywhere across their global network. The vast amount of collected data over many years allows them to produce sophisticated results from complex data patterns and translate that into an accurate picture of a machine’s health. They can accurately monitor assets across process operations, and the rich datasets allow test and inspection companies to offer new services, such as predictive maintenance and data-based services across a range of sectors.

A number of new technology entrants have emerged which seek to offer real-time, onsite results – however, without access to large historical databases, the technology is limited by its accuracy.

The model has proved resilient during Covid-19, with the larger players reporting revenue declines of only 5% as manufacturers continue to rely on services and increasing data and analytics to ensure production and supply chain uptime.

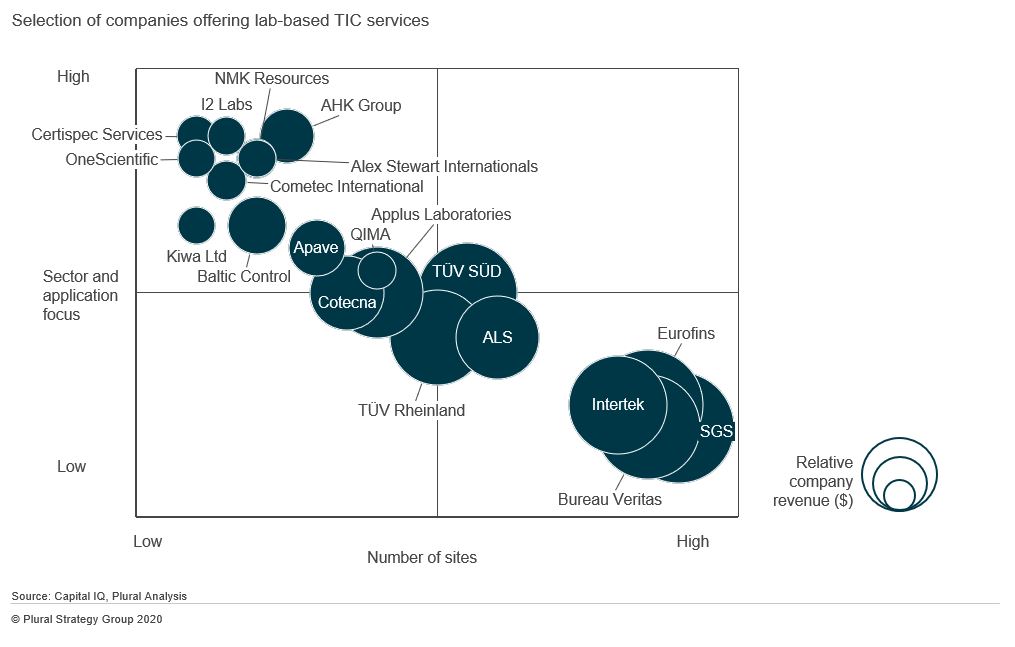

The lab-based test and inspection market remains fragmented, but the top players are consolidating the market with M&A

The industrial lab-based test and inspection market is highly fragmented, with the largest three players – Intertek, Bureau Veritas and SGS – holding a combined market share of less than 20%. The market is still comprised of thousands of accredited labs, the large majority of which belong to companies with less than 100 employees offering specialised services. These smaller companies are typically highly focused on a specific sector/application and are focused on serving end-users in a specific geography that require local labs.

There has been rapid market consolidation occurring with Intertek, Bureau Veritas, SGS SA and Eurofins carrying out more than 200 acquisitions in the past five years as they aim to expand their geographic and market coverage and service offering.

How is the lab-based test and inspection business model evolving?

Lab-based test and inspection services are continuously adapting their proposition by further developing a global network and improving customer experience through intelligent tools and technologies. Evolving the model through digital technology investment outside of the lab is a key strategy to embrace the opportunity to get closer to the customer through real-time, predictive solutions rather than allow it to become a threat.