Water management is an attractive platform for both technology corporations and investors due to its strong secular trends, regulatory and technology disruption, and fragmented landscape.

First version published June 2020, updated October 2021

What is driving water technology investment?

Water technology investment is driven by strong underlying drivers, including:

- New infrastructure and needs to modernize networks – urban population growth and aging infrastructure is driving government investment in both developed and developing markets.

- Cost base and efficiency of water usage – technology and analytics integration decreases water waste and usage.

- Environmental factors

What are the end markets for water management technology?

There are four major end markets for water management products:

- Agriculture

- Industrial

- Municipal

- Residential and commercial

Agriculture

Agriculture has experienced a recession since 2014 which has suppressed investment in equipment. Long term agricultural output needs to double by 2050 and agriculture will face increasing competition for water from other needs such as urban growth. This means it needs to use water more efficiently.

- Automated irrigation – Irrigation is a focus point for water scarcity. As the largest withdrawal of water globally, new technologies that increase efficiency and output offer significant growth potential

- Aquaculture – Aquaculture is transitioning into more efficient farmed methods requiring storage and water treatment solutions

Industrials

Waste regulation and high purity are driving investment in the industrial segment:

- Regulatory pressure on industrial wastewater is increasing investment into treatment and re-use technology.

- There is high growth potential in treatment technology due to the level of purification needed in Electronics, Pharmaceuticals and Food and Beverage.

- Wash-down and general water usage is a huge production cost in sectors such as food and beverage.

- Desalination technology gives the opportunity for coastal industries to move away from freshwater.

Municipal water and wastewater investment

- Urban population growth, water scarcity and ageing infrastructure are strong investment drivers.

An estimated $14bn of water is lost by utilities. - Corrosion of old copper and lead pipes is leading to water pollution during transportation to homes.

- An estimated $1tr in investment is needed in the US pipe infrastructure over the next 25 years.

- High growth potential in technology solutions to increase water efficiency and predict pollution occurrence.

- However, growth is highly dependent on municipal spending which is typically reliant on central government funding.

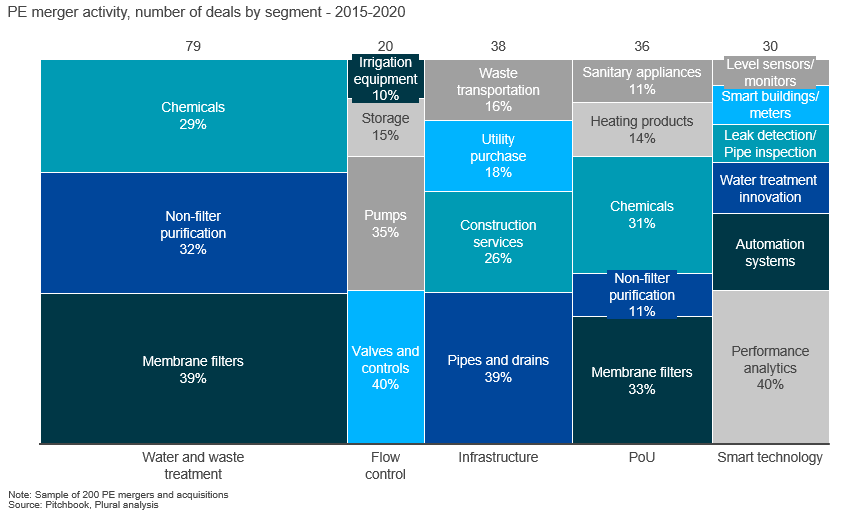

What are the key water management technology segments?

The water management technology sector can be broken up into 5 major categories with sub-product groups that are sold across multiple end markets:

- Water and waste treatment

- Flow control

- Infrastructure

- Point of Use (PoU)

- Smart technology

Water and wastewater treatment products offer investment opportunities in strong growth markets with high levels of fragmentation. Point-of-use treatment systems will likely be an attractive market due to high market fragmentation and growing demand. Smart water technology is a cause of high disruption across many markets but is quickly becoming consolidated among major players.

Water and wastewater for Private Equity (PE) investors

Water and wastewater treatment has been an attractive area of investment for PE investors since 2015. There is significant activity in both large scale and PoU: