After years of stagnation, US water infrastructure investment has started to see growth across segments, the question for investors and operators is what is fundamentally driving this and whether it will continue.

The North American water infrastructure market appears attractive with fundamental secular drivers, notably extensive networks of aging infrastructure which need to be upgraded. However, historically that doesn’t necessarily translate to investment.

Plural tracks five leading indicators to understand and predict infrastructure spending:

- Construction spend and general health of the economy

- Municipal budgets and water rates

- Funding from municipal bonds

- Federal mandates and enforcement programs

- Federal funding

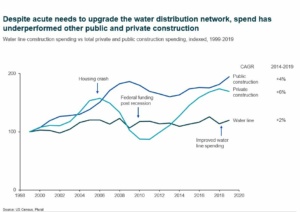

Pre-2008, predicting market direction was a lot simpler – mostly aligned to housing and construction. Since the housing collapse, the market has been mostly reliant on two sources of funding: 1. Municipal budgets and rate hikes and 2. Funding from municipal bonds. Typically, municipal budgets are tight and most municipalities, outside of major cities, are reluctant to hike up water rates and struggle to self-fund infrastructure projects. Therefore, municipal bonds which are benefitting from low interest rates and several other positive factors, become the key source of funding for municipalities. However, this source of funding alone is not enough to really drive major upgrade projects.

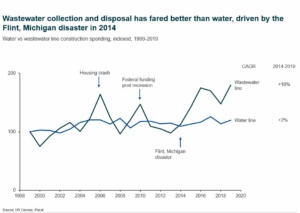

By far the most significant driver of investment is federal mandates and federal funding, typically driven by economic downturns or disasters. The Flint, Michigan disaster in 2014 caused huge public awareness and forced the federal government to act with funding and much stricter mandates – driving spend in the wastewater / stormwater collection and disposal segment.

The key trigger of the recent uptick in spend is a combination of a positive municipal bond environment but importantly renewed federal funding, specifically WIFIA – a program set up in 2017 specifically to fund water infrastructure projects. Funding for WIFIA significantly increased in 2018 and 2019.

In conclusion, there are several indicators worth tracking to understand the direction of water / wastewater infrastructure spend in North America. The reality is that although positive structural drivers exist, actual spend for major projects remains heavily reliant on federal support, which historically has been driven by major events or economic pressure. Given the acute need to upgrade the existing network we expect the new federal funding program (WIFIA) to continue to support an uplift in investment across key water / wastewater infrastructure segments.

Want to know more how we help clients in the industrial technology sector?

Plural’s industrial team has extensive expertise in the water / wastewater infrastructure market across North America, Europe and Asia. We work closely with manufacturers in the market and investors.

Browse our insights and case studies within the sector for more details here.

Alternatively, contact our expert team by submitting the form below.

[contact-form-7 id=”761″ title=”Let’s Talk”]